Setting the record straight on premium-financed IUL

If you sell life insurance, you already know indexed universal life. You know the flexible premiums, the downside protection, the cash value tied to an index like the S&P 500, and a death benefit that can serve a family for decades.

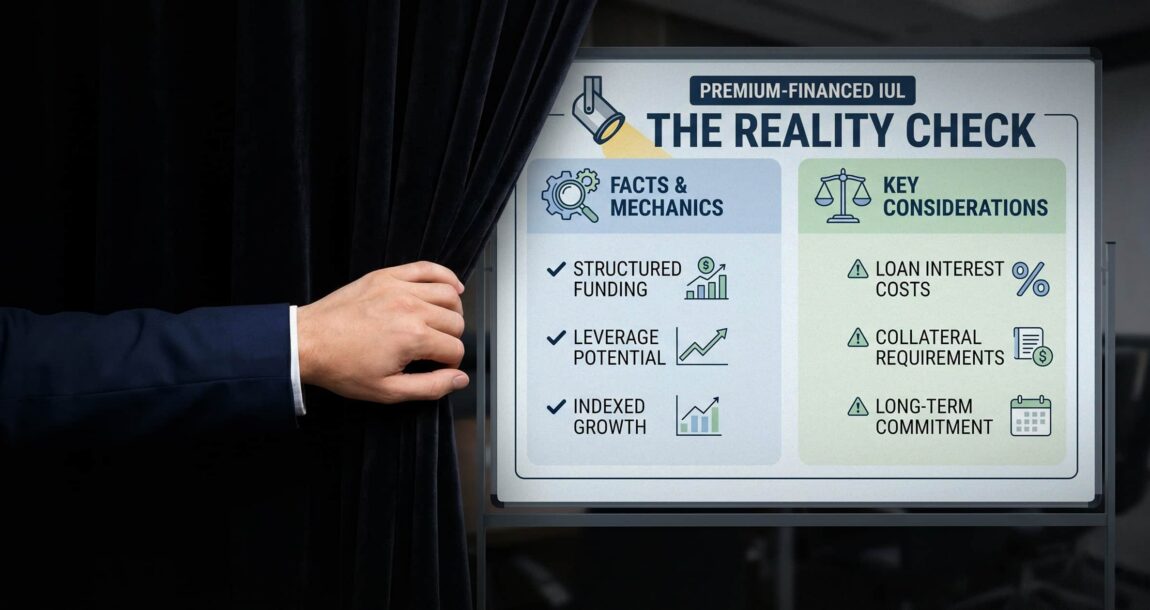

What you may be less familiar with is what happens when a high net worth client uses borrowed money to fund that policy, a strategy known as premium financing, and why that strategy has become the subject of some of the most charged coverage in the insurance trade press in recent memory.

Here is the short version of how it works. A client with a significant estate-planning need, typically a projected estate tax liability of millions of dollars, takes out a loan from a third-party lender to fund the premiums on a large IUL policy. The policy is pledged as collateral, along with other personal assets. The client pays interest on the loan, typically out of pocket each year. The policy accumulates cash value over time, and the design assumes the cash value will eventually retire the loan principal, usually within 15 to 20 years.

What remains is a fully funded life insurance policy that provides a tax-advantaged death benefit to address the estate tax exposure the client sought to address in the first place. This is not a funding strategy for the average policyholder. It is a sophisticated planning approach for clients with complex balance sheets, illiquid assets and real, quantifiable estate-planning needs.

It is also a strategy that has recently drawn significant scrutiny. A Financial Industry Regulatory Authority arbitration panel ordered a former broker to pay $2.25 million to his client’s estate. The client’s family alleged that the broker “pushed” a premium-financed IUL arrangement on the client that exposed them to outsized risk, resulted in a "massive" commission to the agent and caused significant losses.

Cases such as this one, alongside a wave of critical trade coverage that frames premium-financed IULs as a commission-driven debt trap, put advisors in this space on the defensive. Some are pulling back from the strategy entirely. Others are struggling to respond to client questions shaped by negative headlines.

That pullback is understandable. It is also, in most cases, premature and short-sighted. The cases driving the negative coverage are real, but they are problems of execution and disclosure, not of the strategy itself. There is an important distinction between the two, and it is one every advisor who works with high net worth clients must clearly understand. With that context in mind, let's address the three misconceptions doing the most damage right now.

Misconception 1: Premium-financed IUL Is "free insurance"

You have probably heard this framing. The idea is that the policy's cash value growth eventually repays the loan, so the client gets coverage without effectively spending their own money. It is a catchy line. It is also completely wrong.

Clients pay interest on the loan, typically out of pocket, annually. That is a real, ongoing cost. Any advisor or client who believes that deferring or skipping loan interest carries no negative consequence is mistaken. In almost all premium-financed structures, the client pays interest out of pocket. Focusing on the small subset of cases where interest is never paid, without that context, is misleading and detracts from the strategy's genuine value.

For clients using premium-financed IUL as an estate-planning tool, this framing misrepresents the actual rationale for planning. These are high-net-worth individuals with projected estate tax liability or significant liquidity needs who are making a deliberate cost-benefit decision. Many hold highly illiquid assets, and life insurance addresses the worst-case outcome at death in a way few other tools can. The relevant question is whether the interest cost is justified by the estate tax exposure being addressed and whether it compares favorably with out-of-pocket premiums that are often many times higher. A straightforward presentation covers the loan amount, the interest rate, the alternative premium cost without financing, and the estate-planning needs the structure is designed to meet. Complexity is not the problem at the high-net-worth level. Context is.

Misconception 2: IUL illustrations are uniquely unreliable

Critics who argue that illustrated IUL returns are unlikely to be realized under real market conditions often do so without applying the same standard to the rest of the product universe. That inconsistency matters.

IUL illustrations are governed by Actuarial Guideline 49, a regulatory framework that grounds assumptions in historical index performance. That is not a marketing claim; it is a regulatory requirement. Meanwhile, whole life dividend scales have declined steadily over the past two decades, yet that is rarely described as a systemic product problem. Variable universal life policies can illustrate returns of 8% or more without attracting the same scrutiny. If the standard is going to be applied to IUL, intellectual honesty requires applying it across the board.

For clients using premium-financed IUL in an estate-planning context, the success criteria differ from those used in a retirement-income design. An estate-planning strategy is evaluated against the death benefit, its cost and the efficiency of addressing the estate tax liability through the policy versus alternatives. Conflating that objective with a retirement accumulation narrative, then criticizing the illustration for not meeting retirement income benchmarks, produces conclusions that do not apply to the strategy being evaluated.

Misconception 3: Early underperformance equals policy failure

This may be the most consequential misunderstanding in circulation right now.

No life insurance policy is designed to be evaluated in year five. This is especially true for estate-planning strategies, where the policy's purpose is to deliver a death benefit that addresses estate tax exposure at the point of wealth transfer. The relevant measuring sticks are whether the death benefit is in force and whether the need still exists. Given market conditions over the past 10 to 15 years, most IUL policies have outperformed their illustrated projections. Arguments about future failure are speculation, not evidence.

When early-year performance does not match the illustrated projections, the correct response is a review conversation: examine interest rate changes, index performance and the client's financial picture, then adjust the design where appropriate. Clients who find themselves strained because they stopped paying interest and can no longer meet collateral requirements are not victims of a flawed product. They are experiencing the consequences of an execution problem that almost always stems from inadequate expectation-setting at the point of sale.

The real differentiator: How you present, not what you sell

Complaints about the premium-financed IUL space rarely stem from the strategy itself. They stem from the gap between what clients believed they were told to expect and what they experienced, and, more fundamentally, from a disconnect with the coverage's original purpose. In most cases, the underlying need for life insurance has not changed.

Estate planning is where premium-financed IUL does its most consequential work. A properly structured policy can preserve assets, create a tax-advantaged transfer mechanism, and provide certainty around an estate tax liability that would otherwise significantly reduce what the family passes on. That outcome deserves to be communicated clearly and in the client's terms.

The cases making headlines, including the FINRA arbitration mentioned earlier in this article, share a common thread: a breakdown in disclosure, expectation-setting and comprehension at the point of sale. Those are execution failures. The strategy they involve is not inherently broken. Understanding that distinction is the starting point for every financial professional who wants to serve high net worth clients in this space with confidence and integrity.

© Entire contents copyright 2026 by InsuranceNewsNet.com Inc. All rights reserved. No part of this article may be reprinted without the expressed written consent from InsuranceNewsNet.com.

The Annuity Evolution: New Rules, Smarter Tech

Millennials are ready to bring their advisor to the family table

Advisor News

- Why advisors should be talking about life settlements

- Millennials are ready to bring their advisor to the family table

- How healthcare inflation can eat up a client’s retirement income

- Global economy ‘resilient’ in the wake of massive disruption

- Cryptocurrency legislation takes one step forward with bipartisan support

More Advisor NewsAnnuity News

- NAIC regulators continue pushing for annuity illustration updates

- Wink: Flat first-quarter annuity sales fall just short of $100B

- 26North Re Agrees to Acquire 100% of Independent Insurance Group

- Matthew Michelini named Athene president, with an eye on annuity growth

- Lincoln Financial Announces Executive Leadership Transitions

More Annuity NewsHealth/Employee Benefits News

- Tom Campbell: We're paying too much for poor health care

- Self-pay and dental care: Can paying cash without insurance help you save?

- These Connecticut-based companies made this year's Fortune 500 list with revenue up to $275 billion

- Surgery transforms epilepsy patient's life

- Arizona AG accuses health insurance companies of illegal price fixing

More Health/Employee Benefits NewsLife Insurance News

- Prudential announces more layoffs as insurer continues to restructure

- Pradip Patiath Joins Securian Financial Board of Directors

- Over $107 million in life insurance benefits located for Tennesseans in 2025

- Study Data from National Institutes of Health Provide New Insights into Law and the Biosciences (Taking actuarial fairness seriously: what is required for the ethical use of genetics in insurance?): Legal Issues – Law and the Biosciences

- 26North Re Agrees to Acquire 100% of Independent Insurance Group

More Life Insurance News